Klarna vs Clearpay on Shopify: Which BNPL Should Your UK Store Use in 2026?

Klarna vs Clearpay on Shopify for UK stores in 2026. Real fee ranges, settlement timing, customer mix, returns flow, and a decision framework by AOV.

Key takeaways:

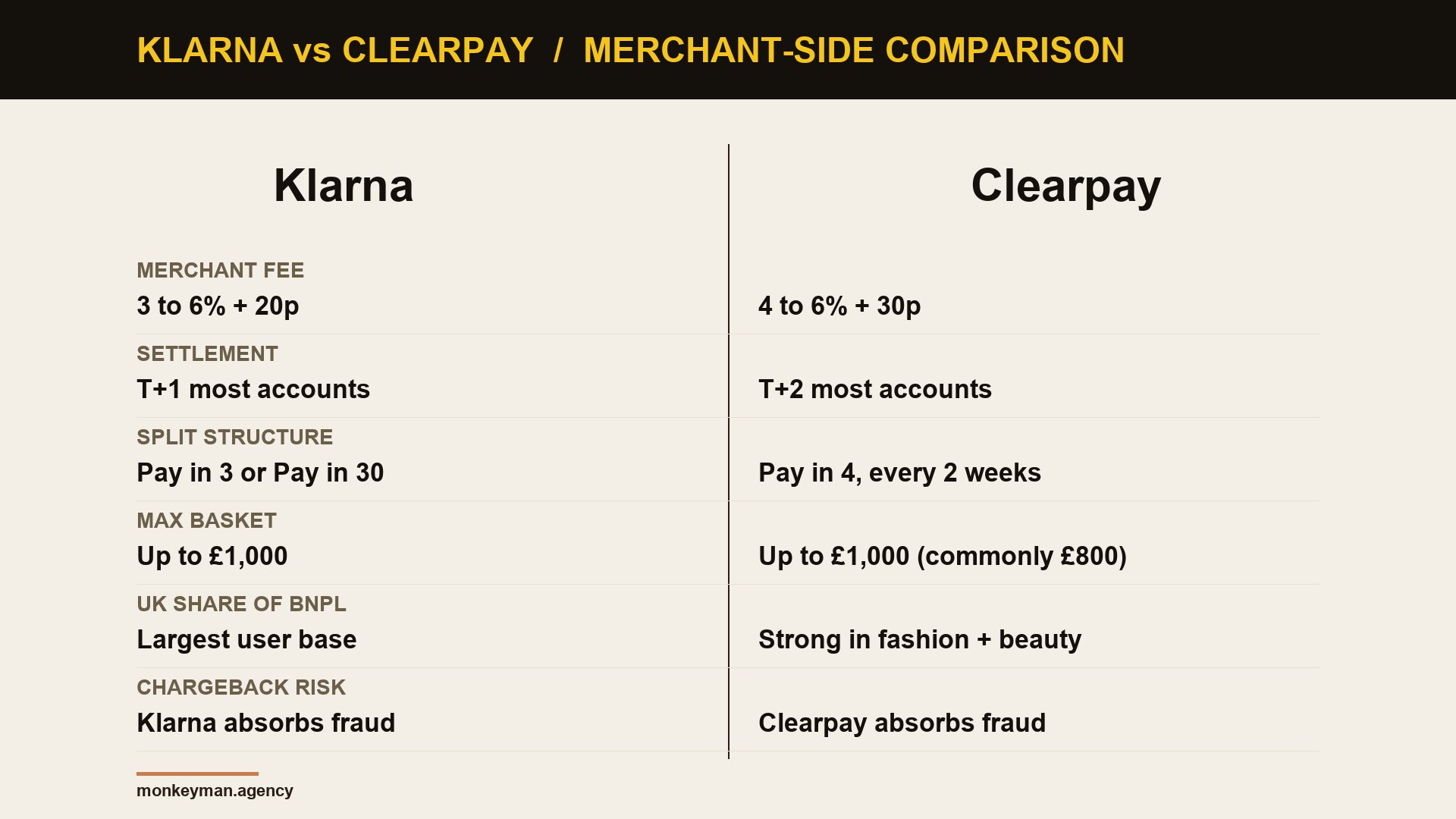

- Klarna and Clearpay both plug into Shopify cleanly, but the merchant fee ranges are wider than their marketing pages suggest, 3 to 6% for Klarna and 4 to 6% for Clearpay, with volume negotiation real once you cross around £40k per month per provider.

- Klarna carries the bigger UK user base across categories. Clearpay punches above its weight in fashion, beauty, and accessories under £150.

- Settlement is T+1 for most Klarna accounts and T+2 for most Clearpay accounts, which matters more than the fee delta on tight cash cycles.

- Both providers absorb chargebacks and fraud on approved orders. Your loss exposure shifts to refunds and partial returns, which behave differently in each portal.

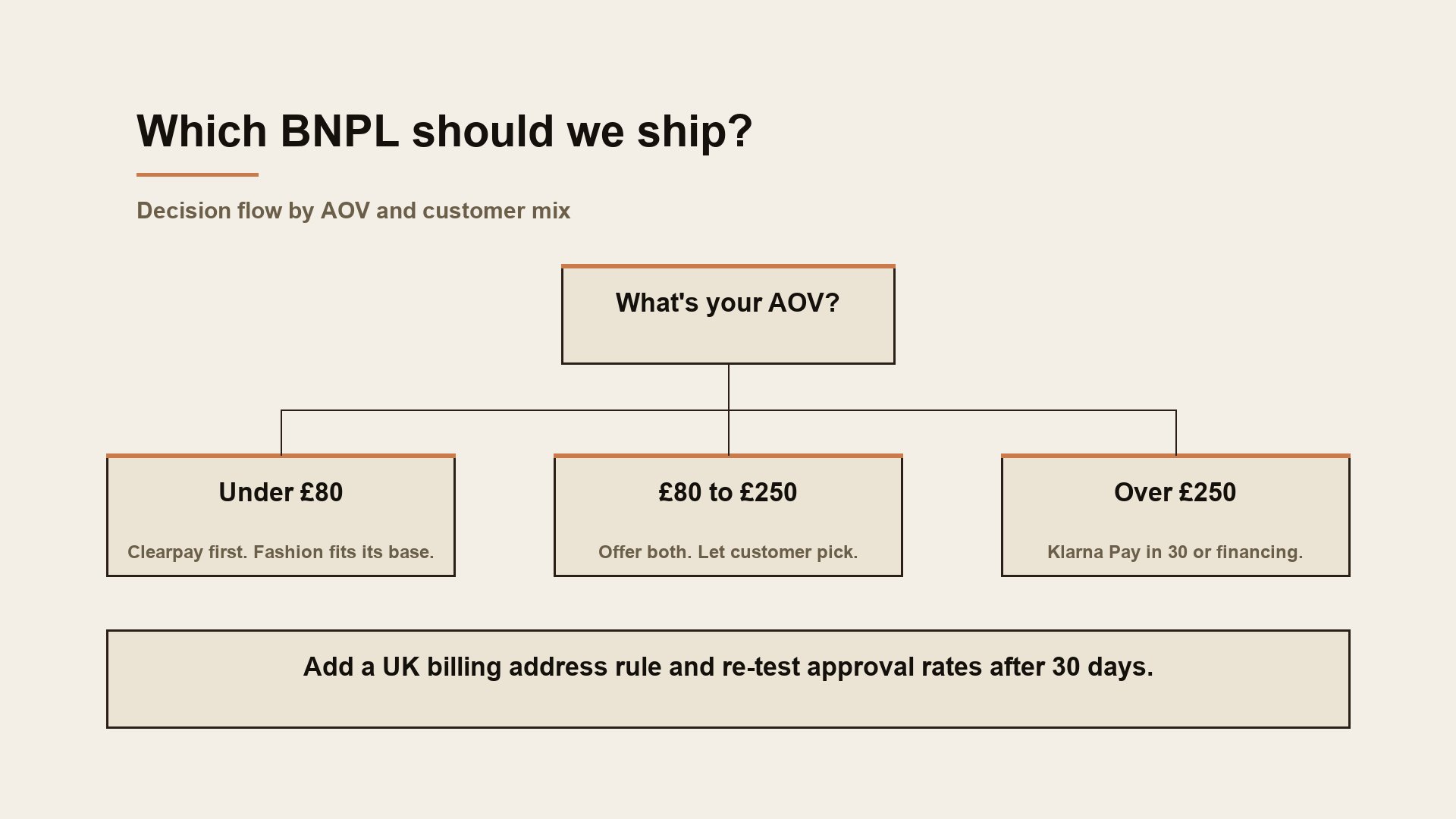

- Below an AOV of around £80 we usually ship Clearpay first. Above £250 we ship Klarna first. In the middle, we ship both and let the customer pick.

A Manchester streetwear brand asked us last summer whether Clearpay was worth keeping if they were already on Klarna. Their AOV was £74. Klarna take rate at checkout was 9%. They were paying roughly 4.4% blended and wondering if a second BNPL was worth the work. We ran a four-week test. Clearpay added a clean 6.2% of revenue, almost none of it cannibalised from Klarna, and lifted conversion on under-£100 baskets by 11%. Their finance lead’s first question after the test was the same one we hear most: if we have to pick one, which one. Fair question.

This guide is for UK founders making that pick in 2026. We run Shopify Payments, Stripe, and both BNPL providers across our active client list. What follows is how we actually compare them, not the spec-sheet version.

How each integrates with Shopify

Klarna ships as a payment method through Shopify Payments in the UK. You enable it inside Settings, Payments, alternative payment methods. There is also a standalone Klarna for Shopify app for the on-site messaging widget (the “from £12.33 a month with Klarna” line) on product and cart pages. We install both. The integration inherits Shopify’s risk checks and the merchant account stays inside Shopify Payments reporting.

Clearpay has its own Shopify app and also surfaces as a payment method through Shopify Payments. We install the official Clearpay app for the on-site messaging and the dynamic instalment breakdown on PDPs. Without that messaging block, Clearpay sells about a third less in our test data, because shoppers do not know what they qualify for until they hit checkout.

JS load behaviour matters. The Klarna messaging widget defers cleanly and adds about 18 KB of compressed JS. The Clearpay PDP widget historically loaded a heavier script that hit Lighthouse scores on slow theme builds, so we wrap it in a requestIdleCallback shim on themes where Web Vitals are tight. On Dawn or a clean 2.0 theme, neither widget should push LCP past 2 seconds.

Fees and merchant commission, honestly

Both providers publish “from” rates that nobody actually pays at year one. Here is what we see across our UK book in 2026:

- Klarna Pay in 3 and Pay in 30 land between 3.29% and 5.99% plus 20p per order. New merchants under £15k per month sit at the top of that range. Cross £40k per month and renegotiate, 3.49 to 3.99% is normal. Klarna’s UK sales team negotiates, and we have seen 60 to 80 basis points come off.

- Clearpay Pay in 4 lands between 4.0% and 5.99% plus 30p per order. Top fashion brands break under 4%, but Clearpay’s floor is harder to push than Klarna’s. We have not seen a Clearpay deal under 3.8% in 2026.

Neither charges currency markup since you bill in GBP, and there is no monthly platform fee on either standard Shopify integration. Budget 4 to 5% blended in year one, then renegotiate at the 12-month mark with real volume in hand.

The customer-facing experience

Klarna offers three core flows in the UK: Pay in 3 (three equal payments, no interest, first at checkout), Pay in 30 (a single payment 30 days after delivery, no interest), and Financing (6 to 36 month plans with interest, used on baskets above £200). Pay in 3 is the volume driver. Pay in 30 converts well for beauty and replenishment, because the customer pays after they use the product. Max basket for Pay in 3 sits at £1,000 for most approved customers.

Clearpay offers Pay in 4: four equal payments, the first at checkout, the rest fortnightly. There is no Pay in 30 equivalent and no UK financing product at scale. Max basket caps land around £800 to £1,000 depending on the shopper’s Clearpay history.

Pay in 4 spreads over six weeks, which fits the pay cycle of a 22 to 32 year old in the UK. Pay in 3 settles in roughly two months. If your customers skew younger and are paid bi-weekly, Clearpay tends to land. If they skew older and paid monthly, Klarna’s Pay in 30 wins on conversion because it aligns with payday.

UK market share and category fit

Klarna is the largest BNPL in the UK by active users and merchant count. Our blended share across stores running both is roughly 65% Klarna, 35% Clearpay, but variance is huge by vertical.

Clearpay over-indexes in fashion, beauty, accessories, and footwear under £150. We run two skincare clients where Clearpay is the bigger of the two at checkout, despite Klarna having more UK users overall. The reason is brand association: Clearpay (Afterpay outside the UK) built its brand inside fashion influencer marketing in 2020 and 2021, and that stuck.

Klarna over-indexes in homewares, electronics, fitness, travel, and food and drink. Once the basket goes over £150 or the customer wants to pay after delivery, Klarna takes more share.

Supported industries and merchant approval

Both providers publish “restricted industries” lists with similar shape: no firearms, no adult content, no high-risk financial services, no offshore gambling. Friction at approval sits in the grey-area categories: CBD, vapes, supplements making health claims, and firearms-adjacent outdoor brands.

For supplements we have approved both providers on stores selling within MHRA-compliant claims, with Clearpay slightly more conservative on muscle-building stacks. For CBD, Klarna has approved a few clients in the past 12 months. Clearpay has been a hard no on CBD throughout 2026.

Approval timelines: Klarna runs 5 to 10 business days, Clearpay 7 to 14. Both ask for company registration, six months of statements, a director ID check, and a store URL with terms and returns published.

Fraud handling and chargeback flow

Both providers absorb fraud on approved orders. Once Klarna or Clearpay approves a customer for an order, that order pays out to you whether the customer completes their instalments or not. The provider eats the credit risk.

What comes back to you is the return, the refund, and the partial cancellation. These are not chargebacks in the card sense, but they flow through the provider portal. Klarna handles partial refunds cleanly through a per-line-item interface. Clearpay’s portal also supports partial refunds, but the UI has historically been slower for stores running 200+ refunds a month, and we have moved two clients to a Shopify-app-driven refund flow because of it.

Chargeback risk in the card-network sense is essentially zero on both, because the customer’s payment instrument is the provider, not their card. You still get refund disputes where a customer claims they returned an item they did not. The dispute flow on both providers is email-based and resolves in 5 to 15 days.

GBP, Apple Pay, and Shop Pay coexistence

Klarna and Clearpay settle in GBP for UK merchants, no FX. Apple Pay and Google Pay continue to work as accelerated checkout options alongside both BNPL providers. We keep all three buttons visible above the form on the cart page. Shop Pay sits in the express checkout strip and does not conflict with Klarna or Clearpay, though we have seen 2 to 4% of customers tap Shop Pay first, then back out and switch to BNPL at checkout. Do not hide Shop Pay to push BNPL.

The order on the checkout payment method list matters more than people realise. Shopify sorts alphabetically by default, which puts Clearpay above Klarna. We override the order to put the higher-take-rate provider first, using the alternative payment methods sort setting inside Shopify Payments.

Settlement timing

Klarna settles T+1 for most UK accounts. The order pays in on the next banking day after capture. There is a 1 to 2 day rolling reserve on new accounts that drops away after 60 to 90 days of activity.

Clearpay settles T+2 for most UK accounts. The single-day difference compounds when you are running a tight cash cycle on inventory, especially for stores doing six-figure monthly revenue where one rolling day equals real working capital. If cash conversion is your bottleneck, this is a tiebreaker.

Returns and refunds through each provider

Returns are where most operational pain happens. With BNPL, you trigger the refund in the provider’s portal, not in Shopify Payments.

Klarna’s flow: log into the merchant portal, find the order, refund full or per-line. Remaining instalments cancel, already-paid instalments refund to the customer’s card or bank in 3 to 5 business days.

Clearpay’s flow is similar: portal login, find the order, refund full or per-line. Paid instalments refund in 3 to 7 business days. The Clearpay portal search is slower than Klarna’s, and for stores doing high refund volume we recommend using the official Clearpay app on Shopify to trigger refunds from inside your admin.

Partial returns work on both. Exchanges work on neither directly, you process them as refund plus new order. We document the returns SOP for every client moving above 100 BNPL orders per month.

When to offer both, and when to offer one

Two BNPL providers means two integrations, two portals to refund through, and a slightly busier checkout. The question is whether the second provider adds enough net new revenue to justify the operational overhead.

In our test data across 14 UK stores in 2024 and 2025, adding the second BNPL provider added 5 to 11% incremental checkout revenue with low cannibalisation. The exceptions: stores under £25k per month where a second portal is not worth the lift, and stores selling almost entirely above £400 AOV where Pay in 4 does not unlock new behaviour.

For everyone else, run both.

A decision framework by AOV and customer mix

We use a simple AOV-led decision when a client asks us to pick one. The shopper mix and category are tiebreakers.

- AOV under £80, customer mix skews under 35. Ship Clearpay first. Pay in 4 is the most natural fit for the basket and the pay cycle. Add Klarna at month 4 if revenue justifies the second portal.

- AOV £80 to £250, mixed customer base. Ship both. Order the checkout list by which one converts higher in your category. If you do not have data, default Klarna first for homewares and food, Clearpay first for fashion and beauty.

- AOV over £250, salaried monthly customer base. Ship Klarna first. Pay in 30 and Klarna Financing are stronger here. And add Clearpay only if your sub-£150 SKUs are a meaningful share of revenue.

One variable overrides the AOV rule: existing brand association. If your influencer marketing already mentions Clearpay, your customers expect to see it at checkout, and removing it hurts conversion. We saw that in the Manchester streetwear test, where Clearpay was a stronger brand signal than the maths predicted.

What this looks like at scale

Past Shopify Plus volume, the BNPL question becomes a portfolio question. You track share by category, traffic source, and acquisition channel. We have one Plus client where 38% of paid social orders go through Clearpay and 12% of email orders go through Klarna, enough variance to influence creative testing budgets. That is the detail we work to once a brand is past £1m annual revenue. Read our take on the UK stack in our shopify development company in the UK guide, and our Shopify Plus build playbook for the migration timeline.

If you want a second pair of eyes on the install order, the fee ranges your provider quoted, or the checkout sort logic, send us your store. We come back inside 48 hours with which BNPL we would ship first and why.

Compare the products directly at klarna.com and clearpay.co.uk. Both will quote you a rate, the number that matters is what they quote at month 13, not month 1.